27 Apr The balloon goes up| 27 April 2022

Written by David Graham, Senior Financial Planner, Mapp Fin CIMA® CFP®

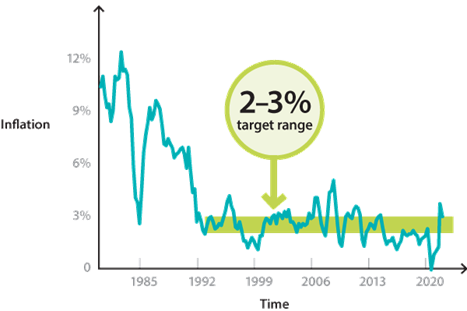

I waited until today’s inflation number was printed before putting ‘pen to paper’. Consensus guestimates were that Q! inflation in Australia would rise to 4.6% (annualised). The actual outcome was 5.1%, with the January quarter alone seeing a rise of 2.2%. Underlying inflation, the data watched by the Reserve Bank, rose from 2.6% p.a. to 3.7% p.a. Clearly, this is above the 2%-3% target range.

You will, no doubt, be assailed by breathless commentary about what this means for interest rates, how the RBA has failed, etc. However, the RBA explicitly states this target range is to be achieved ‘over time, ‘on average’. The nuance is lost in the headlines, but the following illustration provides some context (it does not include today’s number):

Nevertheless, today’s inflation figures do tell us something about the trajectory of interest rates. As I have mentioned previously, market interest rates have been anticipating rising inflation and increases in official interest rates since the beginning of 2022. We have seen an increasing number of central banks raise rates across the world. We were never going to be immune from this; it was and is always, a matter of degrees.

Clearly, the current level of official interest rates, set for the COVID emergency are no longer appropriate. The next RBA board meeting is next Tuesday. The last time they raised rates during an election campaign was in 2007. I would be surprised if they raised rates at this meeting; one month will not alter the longer game they are playing. However, it is almost guaranteed that rates will rise in June. Indeed, I will be unsurprised if they raise the official cash target rate to 0.5% (an increase of 0.4%).

What is important now is whether they can return the rate of inflation to the above range in a timely manner, and without crashing the economy. As with most things, Governments and central banks can only influence at the periphery. For the most part, the current surge in inflation is driven by supply issues. Changing interest rates will not alter the price of oil. Indeed, higher debt servicing costs can suck the air out of broader consumer spending. The consumer will cancel their Netflix subscription if it means making their mortgage payment.

In other parts of the world, mainly the U.S. there is both supply and demand pressures feeding into the inflation rate. Thus, the Federal Reserve is likely to raise rates more quickly. You will recall from previous updates, that the bond markets have been on to this for some time. Long term, market driven, interest rates have risen at the fastest pace in over 30 years.

The Australian consumer is extremely sensitive to interest rate movements. Thus, interest rates do not have to rise very far before some real damage is inflicted. The RBA knows this better than anyone. Thus, I believe they will tolerate inflation persisting above the preferred range for longer than would otherwise have been the case. In short, official interest rates are, in my opinion, likely to rise less than bond markets are currently implying. In this environment, Australian equities ought to be relatively unaffected. However, equity markets are, as we know, affected by a broader range of influences; most notably what happens on ‘Wall Street’. Moreover, the Zero COVID policy currently persisting in China could very well undermine (pun intended) those sectors that have held our markets in good stead to date.

There is also the risk of policy error in Australia. Not by the RBA, but by Government. All sorts of things are said and promised during a campaign, but whoever wins, a fiscal reckoning is nigh. Fiscal policy is a primary contributor to demand driven inflation, so this ought to be the area in which policy is concentrated by the next administration.

I don’t want to get partisan, but I do want to finish with a quick word about those yellow billboards going up. The UAP wants you to believe they will a) ensure your mortgage interest rate is capped at 3% p.a. for five years, b) will levy a 15% tax on iron ore exports to ‘pay off national debt’ c) will make super fund repatriate offshore investments.

Well, we tried capping mortgage interest rates in the early 1980’s. This led to a rationing of loans. Banks won’t lend if they can’t make a profit. The levy on iron ore sounds a bit like the MRRT ~2013. That didn’t go so well. Moreover, the ‘royalty’ proposed is a tax on revenue, not profits. Miners would leave it in the ground until it made sense to dig it up. Making super funds invest all your benefits in Australia is a recipe for lower returns and higher risk. Furthermore, they are going to make you invest more in a market that is dominated by banks and miners, who they are going to squeeze with taxes and interest rate restrictions at the same time. It is simply a recipe for disaster.

You might think the UAP is quite unhinged. However, this has nothing to do with policy. It is about attracting more votes, and with it, more Federal funding. It is a grift. Please point this out to any friends and associates who are less able to detect the manipulation being perpetrated to attract their vote.

Ok, I feel better.

The extent to which global interest rates rise, will determine the longer-term trajectory of equity markets. If they can pull off a ‘soft landing’, particularly in the U.S. earnings can remain strong and with it, valuations. This risk to the equity market is not so much in where interest rates are going, but the tipping point at which monetary policy prompts a recession.

Information current as at 27 April 2022

Disclaimer: the information and any advice provided in this email has been prepared without taking into account your objectives, financial situation or needs. Because of that, you should, before acting on the advice, consider the appropriateness of the advice, having regard to those things.